Learn the best debt management strategies to pay off debt faster, reduce interest, improve your credit score, and achieve financial freedom with practical tips and proven methods.

Debt Management Strategies: 10 Proven Ways to Pay Off Debt Faster in 2026

Managing debt is one of the most important steps toward achieving financial stability and long-term wealth. Whether you’re dealing with credit card balances, student loans, medical bills, or personal loans, having a clear repayment strategy can reduce stress and help you regain control of your finances.

Debt management strategies are practical methods used to organize, prioritize, and repay debt efficiently. Popular approaches include the debt snowball method, debt avalanche method, budgeting, increasing income, and debt consolidation.

The good news is that becoming debt-free doesn’t require a high income—it requires consistency, discipline, and a well-structured plan. This guide explores the most effective debt management strategies to help you pay off debt faster and build a stronger financial future.

Table of Contents

- Why Managing

- Debt Is Important

- Understand Your Current Debt Situation

- Compare the Best

- Debt Repayment Methods

- Debt Snowball Method

- Debt Avalanche Method Create a Monthly Budget

- Increase Your Income

- Avoid Taking on New Debt

- Consider Debt Consolidation Build Healthy Financial Habits

- Common Debt Management Mistakes

- Debt Snowball vs. Debt Avalanche Comparison

- A Sample Debt Payoff Plan

- Psychological Benefits of Becoming Debt-Free

- Frequently Asked Questions

- Final Thoughts

Why Managing Debt Is Important

Effective debt management goes beyond making monthly payments. It creates opportunities for financial growth and reduces the burden of high-interest borrowing.

Benefits include:

- Reduced financial stress

- Improved credit score

- Increased monthly cash flow

- Greater financial flexibility

- Better ability to save and invest

- Improved long-term financial security

The sooner debt is eliminated, the sooner your money can work toward building wealth instead of paying interest.

Understand Your Current Debt Situation

Before choosing a repayment strategy, create a complete inventory of your debts.

Include:

- Credit cards

- Personal loans

- Student loans

- Auto loans

- Medical bills

- Buy Now, Pay Later (BNPL) balances

- Lines of credit

Record the following information:

| Debt Type | Balance | Interest Rate | Minimum Payment |

| Credit Card | $4,000 | 22% | $120 |

| Student Loan | $12,000 | 6% | $150 |

| Car Loan | $8,000 | 5% | $220 |

| Personal Loan | $5,500 | 11% | $180 |

Understanding your complete financial picture allows you to prioritize repayments more effectively.

Compare the Best Debt Repayment Methods

There is no single “best” strategy for everyone. The right approach depends on your personality, motivation, and financial goals.

The two most popular repayment methods are:

- Debt Snowball Method

- Debt Avalanche Method

Both are highly effective when followed consistently.

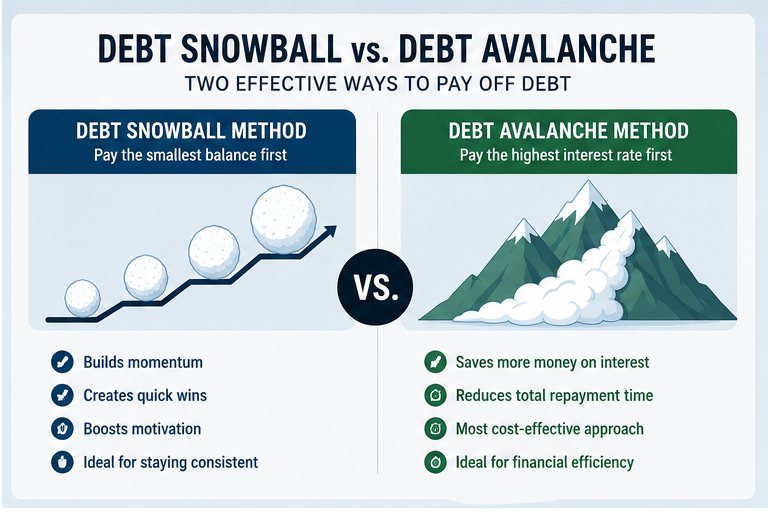

Debt Snowball Method

The debt snowball method focuses on paying off the smallest balance first, regardless of interest rate.

How it works

- Make minimum payments on all debts.

- Direct extra money toward the smallest balance.

- Once paid off, roll that payment into the next smallest debt.

- Continue until all debts are eliminated.

Advantages

- Builds momentum quickly

- Provides psychological motivation

- Creates visible progress

- Encourages consistency

Best for

People who need motivation and quick wins to stay committed.

Debt Avalanche Method

The debt avalanche method prioritizes debts with the highest interest rates.

How it works

- Pay minimum amounts on every debt.

- Put all extra money toward the highest-interest debt.

- Repeat until all debts are paid.

Advantages

- Saves the most money on interest

- Reduces total repayment cost

- Shortens repayment time in many cases

Best for

People focused on maximizing financial efficiency.

Debt Snowball vs. Debt Avalanche

| Debt Snowball | Debt Avalanche |

| Pays smallest balances first | Pays highest interest rates first |

| Builds motivation | Saves more money |

| Creates quick wins | Financially efficient |

| Better for behavioral success | Better for mathematical optimization |

Both methods work. The best strategy is the one you can consistently follow.

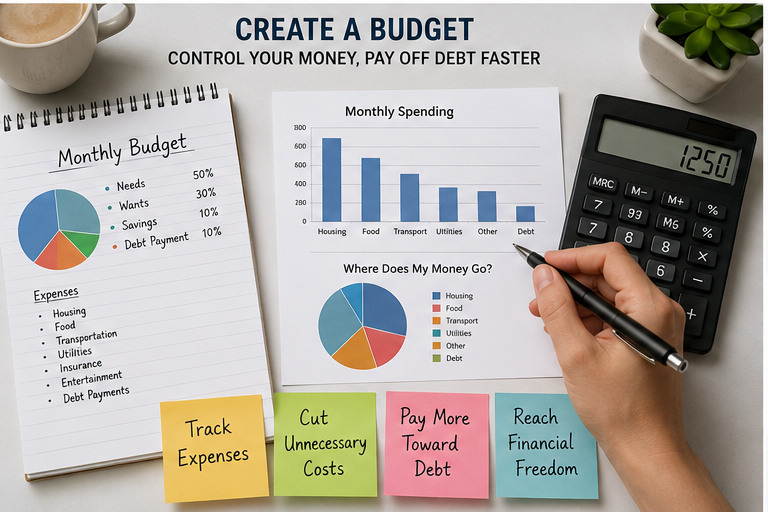

Create a Monthly Budget

A monthly budget ensures every dollar has a purpose and helps identify opportunities to accelerate debt repayment.

Consider reducing:

- Restaurant spending

- Subscription services

- Entertainment expenses Impulse purchases

- Luxury shopping

- Unnecessary travel expenses

Redirecting even an extra $200 per month toward debt can save thousands in interest over time.

Increase Your Income

Increasing your income can significantly shorten your debt payoff timeline.

Ideas include:

- Freelancing

- Tutoring

- Online consulting

- Selling unused items

- Driving for delivery services

- Part-time employment

- Creating digital products

- Starting a side business

Using 100% of side income toward debt can dramatically accelerate progress.

Avoid Taking on New Debt

Many people slow their progress by continuing to borrow while repaying existing obligations.

To break the debt cycle:

- Use credit cards responsibly

- Avoid impulse financing

- Delay unnecessary purchases

- Build an emergency fund

- Follow your monthly budget consistently

Eliminating new borrowing is essential for long-term financial success.

Consider Debt Consolidation

Debt consolidation combines multiple debts into a single loan, often with a lower interest rate.

Potential advantages include:

- One monthly payment

- Lower interest expenses

- Simplified financial management

- Easier budgeting

However, always compare fees, repayment periods, and loan terms before consolidating debt.

Debt consolidation works best when accompanied by improved spending habits.

Build Healthy Financial Habits

Debt repayment is not just about numbers—it’s about changing financial behavior.

Successful individuals often:

- Track expenses weekly

- Save automatically

- Review budgets monthly

- Set measurable financial goals

- Avoid emotional spending

- Invest after eliminating high-interest debt

Healthy habits reduce the likelihood of future debt problems.

Common Debt Management Mistakes

Ignoring Debt

Waiting rarely improves the situation. Interest continues accumulating, making repayment more difficult.

Paying Only Minimum Payments

Minimum payments can extend repayment periods for many years while significantly increasing total interest costs.

Whenever possible, pay more than the required minimum.

Lacking a Budget

Without a spending plan, excess income often disappears into unnecessary expenses.

Budgeting creates financial awareness and accountability.

Overusing Credit Cards

Frequent reliance on credit cards can quickly erase repayment progress.

Use credit strategically rather than emotionally.

Not Building an Emergency Fund

Unexpected expenses often push people back into debt.

Maintaining a modest emergency fund can prevent future borrowing.

Sample Debt Payoff Plan

Imagine you owe:

- Credit Card A: $3,000 (24%)

- Credit Card B: $2,000 (18%)

- Personal Loan: $6,000 (9%)

If you can dedicate an additional $500 per month:

- The snowball method would eliminate Credit Card B first for quick motivation.

- The avalanche method would target Credit Card A first to reduce interest costs.

Either approach is effective as long as you remain consistent.

The Psychological Benefits of Becoming Debt-Free

Financial freedom offers benefits beyond money.

People who eliminate debt often report:

- Reduced anxiety

- Better sleep quality

- Improved confidence

- Stronger relationships

- Increased career flexibility

- Greater ability to invest for retirement

Being debt-free creates peace of mind and opens new opportunities for wealth building.

Final Thoughts

Paying off debt is a journey that requires patience, discipline, and persistence. While the process may seem overwhelming at first, every payment moves you one step closer to financial independence.

By understanding your debt, choosing the right repayment strategy, maintaining a budget, increasing your income, and avoiding new borrowing, you can successfully eliminate debt and build lasting financial security.

Remember, financial success is not achieved through perfection—it is achieved through consistent action over time.

Key Takeaways

- Understand every debt before creating a repayment plan.

- Choose between the debt snowball and debt avalanche methods based on your goals.

- Create and follow a monthly budget.

- Increase your income whenever possible.

- Avoid accumulating additional debt.

- Build healthy financial habits for long-term success.

- Maintain an emergency fund to prevent future borrowing.

- Consistency is the key to becoming debt-free.

Frequently Asked Questions

What is the fastest way to pay off debt?

Many financial experts recommend the debt avalanche method because it prioritizes high-interest debt and minimizes interest expenses.

Which is better: debt snowball or debt avalanche?

Both strategies are effective. The debt snowball method emphasizes motivation through quick wins, while the debt avalanche method focuses on saving money over time.

How long does it usually take to become debt-free?

The timeline depends on your total debt, income, expenses, and repayment strategy. Increasing monthly payments can significantly shorten the repayment period.

Should I save money or pay off debt first?

A balanced approach is generally recommended. Build a small emergency fund while aggressively paying off high-interest debt.

Is debt consolidation a good idea?

Debt consolidation can simplify repayment and reduce interest costs, provided the new loan offers favorable terms and you avoid taking on additional debt.

Can I pay off debt with a low income?

Yes. Careful budgeting, consistent payments, reducing expenses, and earning additional income through side hustles can help accelerate debt repayment even on a modest income.

Does paying off debt improve my credit score?

In many cases, yes. Lower credit utilization and a history of consistent payments can positively impact your credit score over time.

References

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- Fidelity Learning Center

- Investopedia

- Vanguard Investor Education

Related Articles

- Emergency Funds: Why You Need One and How to Build It

- How to Create a Monthly Budget That Actually Works

- 10 Practical Ways to Save More Money Every Month

- Beginner’s Guide to Financial Freedom

- How to Improve Your Credit Score Naturally

- Passive Income Ideas for Beginners

- Budgeting Tips for Families

- Smart Investing Basics for Long-Term Wealth

About the Author

Daniel Hart

Last Updated: June 2026

Daniel Hart is a personal finance writer at ViralStoryHub24, specializing in budgeting, debt management, saving strategies, and practical financial education. His articles focus on helping readers reduce debt, improve financial literacy, and build long-term wealth through sustainable money management habits.